Corporate concentration of the livestock industry

Farmers selling their livestock in Canada over the past forty years have had fewer and fewer buyers. Whether it’s JBS and Cargill for cattle or Maple Leaf and Olymel for pigs, farmers are at the mercy of massive corporations with the power to dictate prices.

One way to quantify this trend is the four-firm concentration ratio [CR-4], which refers to the market share of the four largest firms in a given sector. If the CR-4 is less than 40%, a market sector is considered to be competitive; if CR-4 is above that, anti-competitive behaviour can be expected. In the Canadian beef packing industry, the CR4 has risen from 35% in 1990 to 95% in 2020.

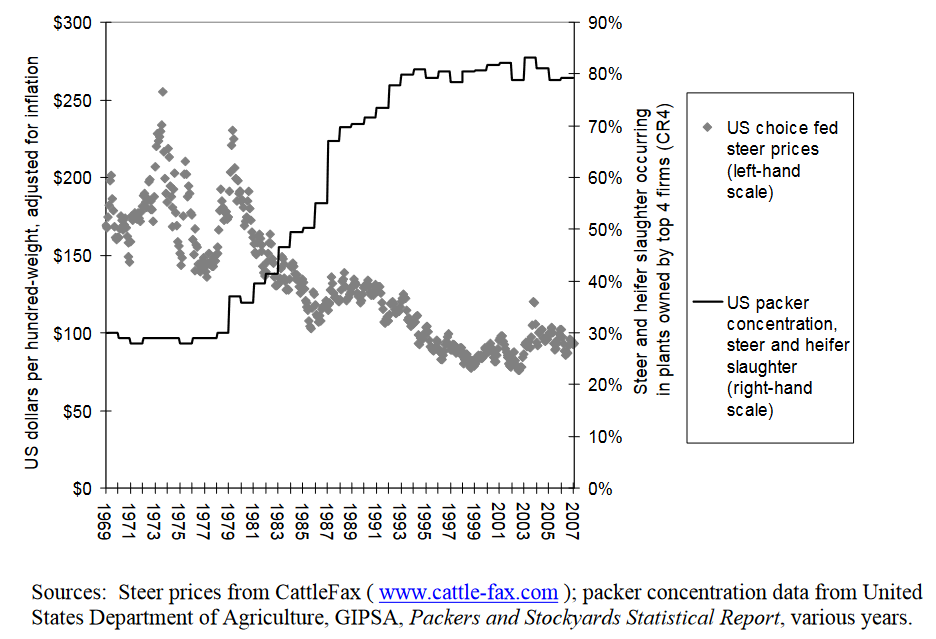

Comparable data from the US clearly demonstrates a correlation between the rise in corporate concentration and the fall of cattle prices when adjusted for inflation.

United States fed (slaughter) steers and US packer concentration, 1969-2006.

Corporate concentration goes hand in hand with vertical integration. Vertical integration is a business strategy where companies control multiple steps of the supply chain. For example, meat packers own not just slaughter plants but feedlots, auction houses, feed mills, and other related businesses.

One key form of vertical integration is captive supply, where meat packers own animals. Captive supply allows them to decide at any given time whether to purchase animals from independent producers or simply to slaughter their own animals. When livestock prices are high, the packers can withdraw temporarily from the market, which puts pressure on farmers to accept lower prices in order to ensure their livestock are sold.

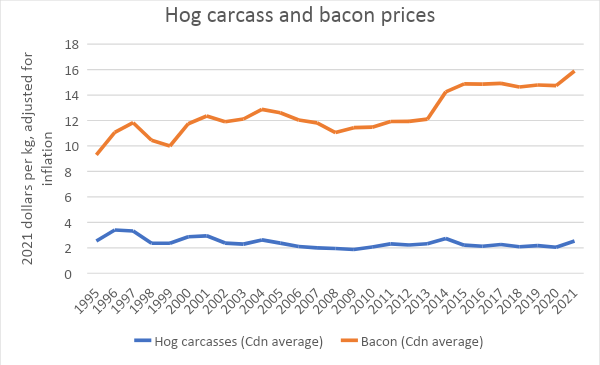

NFU analysis demonstrates that corporate food processors and retailers are using their market power to capture ever-larger portions of money within the food system. For example, the average price consumers paid for bacon in Canada rose by over $6 per kg from 1995 to 2021, even after accounting for inflation. In stark contrast, the average price farmers received for hog carcasses actually fell very slightly over this same period when taking inflation into account. Put simply, consumers had to pay more for their food, and farmers did not receive any of that money.

Source: Statistics Canada Tables 32-10-0077-01 and 18-10-0002-01

Farmers and consumers both suffer as a result of corporate concentration. The solution to corporate concentration is two-fold: limit the power of corporations—meat packers, retailers, etc.—and provide avenues to build the power of farmers through collective marketing agencies.

Supply management has effectively limited corporate power in sectors like dairy and poultry. Marketing boards have the authority to ensure prices reflect the cost of production. For more information on how supply management functions to protect farmers from corporate power, see the NFU website’s supply management section (https://www.nfu.ca/campaigns/supply-management/).

Many provinces used to have single-desk marketing agencies for hogs, where farmers collectively sold their livestock through a central body. These agencies helped counterbalance the power of large meat packers. After the NAFTA deal was signed, provincial single desk hog marketing boards were dismantled in order to promote export-oriented, large-scale, “mega-barn” production. The NFU calls for revitalized single-desk selling and other forms of producer-run orderly marketing in each livestock sector as a way to empower farmers. (https://www.nfu.ca/wp-content/uploads/2018/05/OFPMC-review-of-Ontario-Hog-Board.pdf)

- The Farm Crisis and the Cattle Sector: Toward a New Analysis and New Solutions (https://www.nfu.ca/policy/the-farm-crisis-and-the-cattle-sector-toward-a-new-analysis-and-new-solutions/)

- November 19, 2008

- Cow-calf producers and independent feeders are suffering because they have a problem that is real—packers are paying feedlot operators half of what packers paid those feeders’ parents and grandparents. In turn, cattle feeders are paying cow-calf producers half of what their parents and grandparents received. These half-price cattle are bankrupting family farmers across Canada and creating the most severe crisis in the sector since the Great Depression. This report examines the forces driving this crisis and proposes key solutions to empower farmers rather than corporations. While this report was written in 2008, the dynamics of the sector have only intensified since the Brazilian multinational JBS bought XL Foods.

- The Competition Act as a Tool for Democracy: Fairness for Farmers (https://www.nfu.ca/policy/the-competition-act-as-a-tool-for-democracy-fairness-for-farmers/)

- March 31, 2023

- Livestock markets are just one example of increasing corporate concentration in agriculture. The NFU calls on governments to oppose this trend using all the tools available to them. The Competition Act can be one such powerful tool for balancing the Canadian economy by tempering the positive feedback loops that lead to ever larger, more powerful corporations concentrating wealth and shaping ever larger parts of the economy through their ability to set the terms of commerce as a result of their dominance within the market.

- Gap Continues to Widen between Food Prices that Consumers Pay Retailers and Prices Farmers Receive (https://www.nfu.ca/gap-continues-to-widen-between-food-prices-that-consumers-pay-retailers-and-prices-farmers-receive/)

- April 19, 2023

- Canadians have been struggling to afford groceries. Many farmers have been struggling to make a living. Food retailers and processors, however, have increased their profits. The NFU has prepared a series of graphs that compare the farmgate prices farmers receive for their crops and livestock to the prices that grocers and other food retailers receive for the food they sell. The gap between these two prices—farmgate and retail—has steadily widened over recent decades.

- Grocery Prices are Rising and Farmers’ Share Declining as Corporate Processors and Retailers Take More and More (https://www.nfu.ca/grocery-prices-are-rising-and-farmers-share-declining-as-corporate-processors-and-retailers-take-more-and-more/)

- December 9, 2021

- Op-Ed: Regenerate Canada’s beef sector by addressing corporate concentration (https://www.nfu.ca/op-ed-regenerate-canadas-beef-sector-by-addressing-corporate-concentration/)

- March 4, 2021

- Time to rebuild our meat processing system (https://www.nfu.ca/letter-time-to-rebuild-meat-processing-system/)

- May 14, 2020

- Meat packing concentration makes Canada’s food system vulnerable (https://www.nfu.ca/policy/meat-packing-concentration-makes-canadas-food-system-vulnerable/)

- April 22, 2020

- NFU Submission on Ground Beef Irradiation (https://www.nfu.ca/policy/nfu-submission-on-ground-beef-irradiation/)

- August 15, 2016

- Our beef is not just with Earl’s – a better system is within reach (https://www.nfu.ca/our-beef-is-not-just-with-earls-a-better-system-is-within-reach/)

- May 3, 2016

- Submission to Ontario Farm Products Marketing Commission review of Ontario Hog Board (https://www.nfu.ca/policy/submission-to-ontario-farm-products-marketing-commission-review-of-ontario-hog-board/)

- July 22, 2008

- Comments on the Saskatchewan Meat Inspection Review (https://www.nfu.ca/policy/comments-on-the-saskatchewan-meat-inspection-review/)

- December 9, 2005

- Submission to the Federal Competition Bureau regarding the proposed takeover of Better Beef Ltd. by Cargill (https://www.nfu.ca/policy/submission-to-the-federal-competition-bureau-regarding-the-proposed-takeover-of-better-beef-ltd-by-cargill/)

- June 23, 2005